Strategy faces $8.3 billion Bitcoin Q2 loss as Saylor sells over $200M in BTC

Michael Saylor’s company sold Bitcoin to help fund preferred-stock payouts, testing a model built on years of accumulation.

Quick Take

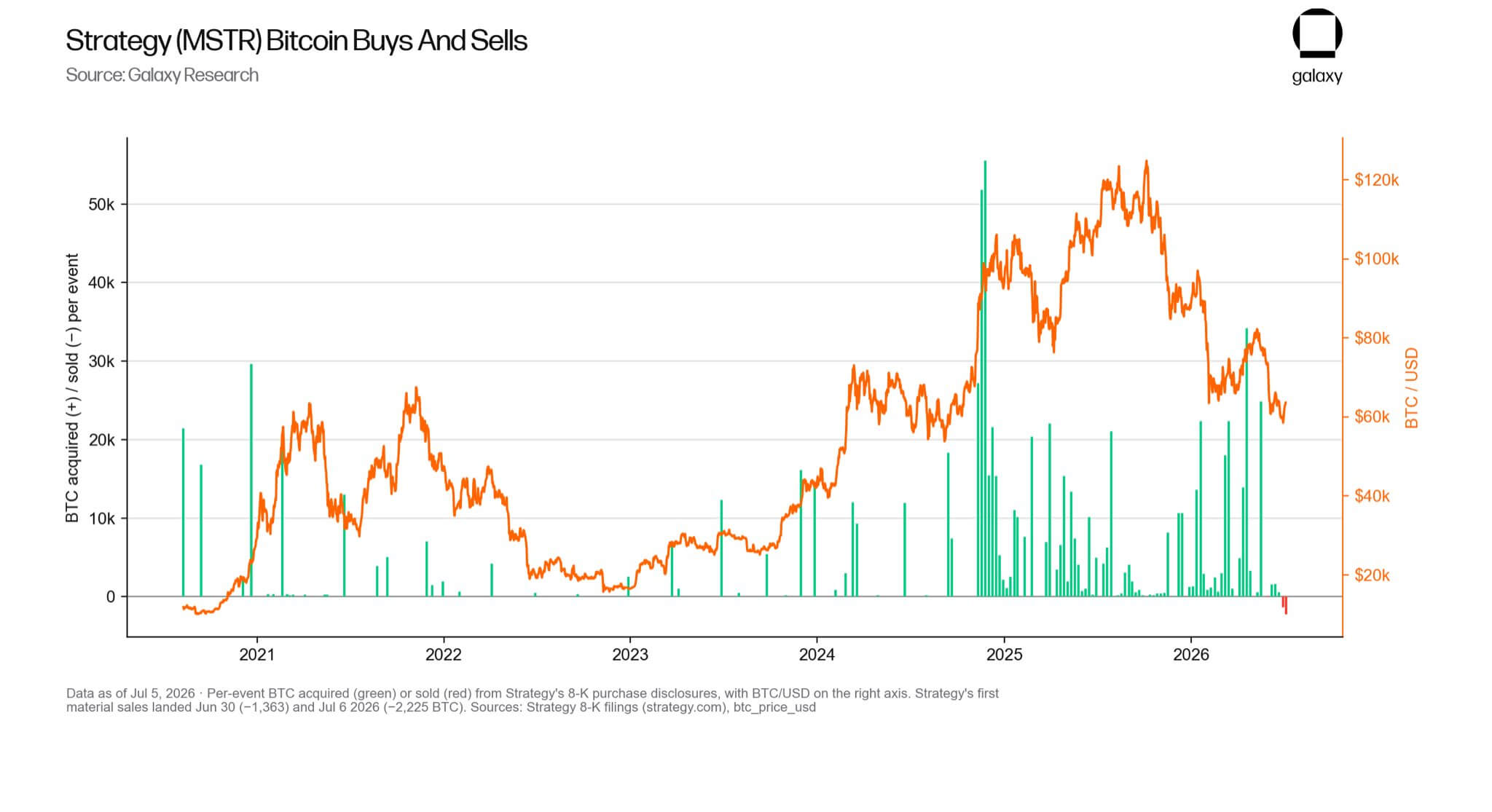

- Strategy sold 3,588 Bitcoin for about $216 million from June 29 to July 5, its biggest sale in years.

- The proceeds funded preferred-stock dividends and replenished dollars reserved for payouts, while Bitcoin holdings still dwarf the sale.

- The move raises a fresh question: whether future cash needs will force more Bitcoin sales when the company is under market stress.

Strategy’s largest Bitcoin sale in years has put new pressure on the corporate treasury model that made Michael Saylor one of the most closely watched figures in digital assets.

On July 6, the company, formerly known as MicroStrategy, revealed that it sold 3,588 Bitcoin for about $216 million between June 29 and July 5.

Per the filing, Strategy sold the coins in two batches. It first sold 1,363 Bitcoin between June 29 and June 30 at an average price of $59,256, followed by another 2,225 Bitcoin between July 1 and July 5 at an average price of $60,773.

With the previous 32 BTC sale, the firm sold a total of 3,620 BTC in the second quarter. However, the firm remains a net buyer of the top crypto, acquiring over 85,000 BTC during the reporting period.

While these BTC sales are small compared with Strategy’s remaining 843,775 Bitcoin, it marked a notable shift for a company long associated with relentless accumulation and a public refusal to treat Bitcoin as a source of cash.

Notably, the company’s remaining Bitcoin was acquired for about $63.69 billion, or an average price of $75,476 per coin.

That means the latest sale took place well below Strategy’s average purchase price.

Blockchain analytics platform Lookonchain estimated the recent BTC sales locked in a loss of more than $55 million, based on the difference between the company’s reported sale price and its historical acquisition cost.

Meanwhile, Strategy disclosed an $8.32 billion second-quarter loss on its digital assets holdings after Bitcoin’s decline during the reporting period pushed the value of its holdings below their cost basis.

It added:

“As of June 30, 2026, the cost basis of the bitcoin held by Strategy exceeded the fair value of its bitcoin holdings. As a result, Strategy will record a valuation allowance against its deferred tax benefit and deferred tax asset associated with the unrealized loss on its bitcoin during the quarter ended June 30, 2026, offsetting these amounts in full.”

Strategy turns Bitcoin into a funding source for its preferred offering dividends

Strategy’s Bitcoin sale marked a shift in how the company uses its reserves.

In the filing, the company stated that the proceeds from the sale of 3,588 Bitcoin would fund preferred stock distributions.

Saylor stated:

These were the Q2 quarterly dividends on STRF, STRE, STRK, and STRD, and the full monthly dividend for June on STRC.

The firm also added that the sales would replenish the portion of its US dollar reserve used for those payments. The reserve, which stood at $2.55 billion as of July 5, is meant to cover preferred dividends and interest on outstanding debt.

Meanwhile, the filing also showed what Strategy chose not to do during the period.

The Saylor-led company did not sell common shares through its at-the-market equity program during the week ended July 5, nor did it repurchase common or preferred shares. Its full $1.25 billion Bitcoin Monetization Program also remains available.

That leaves Bitcoin as a more visible tool in the company’s capital-management playbook. Under the framework, Strategy can sell Bitcoin to rebuild its dollar reserve, pay preferred dividends, service debt and support repurchases of common or preferred stock.

Already, market observers such as Jiang Zhuoer, the founder of the Chinese mining pool BTC.top, have suggested that Saylor could sell more coins soon. Zhuoer noted:

“That MSTR is willing to pay this price can only be interpreted as MSTR gearing up to swing trade with a massive coin position, the 20,000 coins already approved by shareholders will likely all be sold.

In this current bear market phase, MSTR—this relentless buy-buy-buy powerhouse of the bull camp— is about to defect to the sell-sell-sell bear camp. And in the bull market phase that follows, we'll witness the biggest whale of all, dumping hundreds of thousands of coins.”

This complicates what had been a simpler market story. Strategy built its reputation by raising capital to buy Bitcoin. The latest filing shows the reverse can also happen: Bitcoin can be sold to support the financing structure that helped fund the accumulation.

That puts the preferred-stock complex closer to the center of the investment case. Strategy’s preferred securities have reduced its dependence on common-share issuance, but they also created recurring cash obligations that sit ahead of common shareholders.

The structure is easier to sustain when Bitcoin is rising and Strategy’s stock trades at a premium to the value of its holdings. In that environment, the company can raise capital on favorable terms and keep adding to its Bitcoin position.

When Bitcoin falls and the stock weakens, management has to balance three competing priorities: preserving liquidity, avoiding unattractive equity issuance, and maintaining confidence among preferred holders.

The latest sale suggests Strategy is willing to use Bitcoin to manage that balance. That gives the company flexibility, but it also raises a new question for common shareholders: whether future dividends, debt costs, or reserve needs could prompt additional Bitcoin sales during periods of market stress.

Bill Miller IV of Miller Value Partners offered a more favorable interpretation, saying shareholders and Bitcoin supporters should welcome the sale because it creates tax-loss harvesting benefits and helps show ratings agencies that Bitcoin is liquid enough to support corporate liabilities.

That is the new tension inside Strategy’s model. Using Bitcoin to support preferred dividends may help validate the asset's use as collateral in traditional capital markets.

However, it also means Strategy’s Bitcoin holdings are no longer insulated from the cash demands of the company’s own financing machine.

Saylor’s Long-Term Thesis Meets a Near-Term Test

Despite the latest Bitcoin sale and the large quarterly loss, Saylor remains publicly committed to the idea that Bitcoin’s next decade will be shaped by deeper integration with global capital markets.

Over the weekend, Saylor cast Bitcoin as a form of digital capital. In his view, the asset’s future will depend less on changes to the protocol or the old four-year halving cycle, and more on the growth of financial structures built around it: ETFs, corporate treasuries, bank credit, derivatives, collateral markets and sovereign reserves.

That thesis helps explain why Strategy has moved beyond simply buying Bitcoin. The company is trying to build a capital-markets structure around its holdings, using preferred stock, debt, cash reserves and other securities to turn Bitcoin into the foundation for what Saylor calls digital credit.

The latest sale shows the practical side of that vision. If Bitcoin is going to serve as capital inside traditional finance, it must also function inside the routines of corporate finance. Dividends have to be paid. Interest costs have to be serviced. Reserves have to be maintained. Investors across the capital structure have to be reassured.

That creates a tension for Strategy. The more the company succeeds in turning Bitcoin into a productive balance-sheet asset, the less its holdings look like a one-way vault. Bitcoin can support credit products and preferred securities, but it can also be sold when those instruments require cash.

Saylor has argued that Bitcoin itself should remain slow-moving and difficult to change, while innovation develops around it through custody, lending, structured products, settlement systems and institutional balance sheets. Strategy is now testing that argument in public markets.

The company’s challenge is no longer just convincing investors that Bitcoin will rise over time. It must also convince them that a corporate financing machine built around Bitcoin can withstand periods when the asset falls.

Bitcoin is -0.24% over the past 24 hours and currently sits at rank #1 by market cap.

More Bitcoin market context Supply, launch date, volume flow, and price-cycle context.

Where the broader market sits right now

Right now, the total crypto market is valued at $2.21T with $62.21B in 24-hour volume. Bitcoin dominance sits at 58.68%. Explore the market