Bitcoin’s $60,000 support is still a bet on the dollar breaking

Glassnode says Bitcoin’s $60,000 support may need DXY below 99 or 10-year yields near 4.2% before recovery can firm.

Quick Take

- Glassnode says Bitcoin is in a deep discount phase, with over 95% of short-term holders underwater.

- A durable recovery may need the dollar index below 99 or 10-year Treasury yields near 4.2%.

- With DXY above 100 and yields at 4.53%, June CPI and the FOMC may decide if $60,000 holds.

Glassnode's latest Week On-chain report says Bitcoin has entered a deep discount phase, with over 95% of short-term holders underwater and realized losses approaching levels associated with severe capitulation.

The report also notes that a durable Bitcoin recovery is likely to require either the dollar index breaking below 99 or the 10-year Treasury yield compressing toward 4.2%. DXY sits at 100.01, up 2.1% over 30 days, and 10-year yields are at 4.53%.

That frames Bitcoin $60,000 support as a macro-dependent level whose durability hinges on DXY and Treasury yields.

Leverage has been flushed, valuation metrics are deeply discounted, and the dollar-yield setup governing risk appetite is still hostile.

BTC's recovery depends on whether macro conditions loosen, given the FOMC meeting on June 16-17 and the June 10 CPI data.

The on-chain setup

Glassnode's AVIV z-score reached -1.09 before settling at -1.06, placing BTC deep inside an extreme discount band relative to its cyclical mean.

The AVIV ratio compares Bitcoin's spot price with the average cost basis of active investors, excluding miners, and currently sits at 0.80. Short-term holders are near maximum stress, as the Short-term holder MVRV fell to 0.81 before recovering to 0.83, meaning recent buyers are roughly 17% to 19% underwater on average.

Only 3.3% of short-term holders are in profit, against a four-year mean of 55%. Realized-loss behavior is close to severe capitulation, with the STH-SOPR z-score at -1.86, which is a 0.14 standard deviation short of the -2 level that Glassnode associates with severe capitulation events.

BTC absorbed a 7.5% weekly decline to $61,700, and leveraged longs stacked between $64,000 and $70,000 were aggressively cleared as price broke lower, leaving the liquidation profile cleaner than a week earlier.

A discounted, deleveraged market is the setup for a recovery, provided the buyers who absorb that supply actually show up.

| Signal | Current reading | What it says |

|---|---|---|

| BTC weekly move | -7.5% to ~$61,700 | Price has retested the $60K zone under pressure |

| AVIV ratio | 0.80 | BTC trades below active-investor cost basis |

| AVIV z-score | -1.06 | Deep discount relative to the four-year cycle range |

| Short-term holder MVRV | 0.83 | Recent buyers are roughly 17% underwater |

| Short-term holders in profit | 3.3% | Stress is near maximum; four-year mean is 55% |

| STH-SOPR z-score | -1.86 | Close to the -2 severe-capitulation threshold |

| Liquidation zone cleared | $64K–$70K | Leverage has been flushed from the recent range |

Where demand stands

The Coinbase Premium has remained in discount territory throughout the move toward $60,000, indicating that US spot demand faded as BTC sold lower.

Previous pullbacks drew aggressive dip-buying from Coinbase-linked investors; the current correction has drawn none of equivalent scale.

Corporate treasury accumulation, which supported BTC through April and May with daily inflows above $500 million, has slowed sharply since early June, with daily purchases now at a fraction of that pace.

One-week at-the-money implied volatility briefly surged above 60% before settling near 50%, while one-month implied volatility rose from roughly 34% to 45% and six-month implied volatility climbed from around 40% to 44%.

The volatility risk premium is still positive: implied volatility outpacing realized volatility, with options markets pricing more forward movement than recent spot action has justified.

One-month 25-delta skew moved from roughly 11% to 24%, with three-month and six-month skew climbing toward 18% and 14%, respectively. Put buying represented 32.4% of premium over seven days and 35.9% over the most recent 24-hour period Glassnode tracked.

That combination of fading spot demand, slowed treasury accumulation, and options markets heavily priced for downside shows why a discounted market can stay discounted.

| Demand / risk signal | Latest reading | Market implication |

|---|---|---|

| Coinbase Premium | Still in discount territory | US spot demand has not aggressively bought the dip |

| Treasury accumulation | Down sharply from >$500M/day | Corporate demand that supported April–May has weakened |

| 1-week ATM implied volatility | Briefly >60%, now ~50% | Traders are pricing near-term turbulence |

| 1-month implied volatility | ~34% → ~45% | Medium-term risk expectations have risen |

| 6-month implied volatility | ~40% → ~44% | Longer-dated uncertainty is also elevated |

| 1-month 25-delta skew | ~11% → ~24% | Options market is paying up for downside protection |

| Put-buying share of premium | 32.4% over 7 days; 35.9% over latest 24h | Defensive positioning remains dominant |

The macro condition

Glassnode says the inverse dollar/crypto relationship that defined 2022-2023 has reasserted itself.

The report describes DXY above 100 alongside 10-year yields above 4.5% as a configuration that has historically compressed speculative risk premiums.

The 2-year Treasury yield sits at 4.14%, the 10-year at 4.53%, and the 10Y–2Y spread at +0.39%, a curve Glassnode frames as consistent with a late-cycle environment.

DXY gained 0.8% week-on-week and 2.1% over 30 days, a sustained bid that sharpens the liquidity tightening and raises the opportunity cost of holding speculative assets at the margin. When the dollar rises and Treasury yields hold at current levels, Bitcoin competes against a higher risk-free rate with a stronger dollar amplifying the cost.

Glassnode's recovery threshold, defined as DXY below 99 or the 10-year near 4.2%, marks the level at which that headwind reverses meaningfully.

The May CPI data released on June 10 gives the market its first read on whether the Fed's inflation picture has moved enough to alter rate expectations.

The June FOMC meeting on June 16-17 includes a Summary of Economic Projections, making it the most consequential near-term event for the rate path and the dollar's direction. The next CPI release, covering June data, is scheduled for July 14.

Bitcoin's next confirmation or rejection will come from those data points and the bond market's reaction to them, with the on-chain work already done.

| Scenario | Macro trigger | Expected Bitcoin reaction | What to watch |

|---|---|---|---|

| Bull case | DXY breaks below 99 or 10Y yield compresses toward 4.2% | Spot demand returns, Coinbase Premium improves, options skew normalizes | Softer CPI, dovish FOMC projections, lower Treasury yields |

| Base case | DXY holds near 100 and 10Y stays around 4.5% | BTC chops around $60K without a confirmed recovery | Treasury market reaction after FOMC |

| Bear case | DXY stays above 100 and 10Y remains above 4.5% | More recent buyers capitulate; $60K absorbs selling into weak demand | STH-SOPR moving toward or below -2 |

| Black swan | DXY spikes and yields rise further after CPI/FOMC | Macro overwhelms on-chain discount; BTC breaks below support | Strong inflation surprise, hawkish Fed dot plot, risk-off dollar bid |

Two potential paths ahead

If DXY breaks below 99 or the 10-year compresses toward 4.2%, driven by softer CPI, a dovish pivot in the FOMC's projections, or a broader risk-on rotation, spot demand has room to return.

The Coinbase Premium can recover, treasury accumulation can resume, and options skew can normalize.

BTC's on-chain discount sets up a re-rating, and assets that have already completed the deleveraging cycle tend to reprice first as liquidity conditions ease.

If DXY and the 10-year hold their current levels, more recent buyers capitulate. The STH-SOPR z-score approaches or breaks through the -2 severe capitulation threshold, corporate treasury inflows stay suppressed, and the $60,000 zone absorbs additional selling into a demand vacuum.

Bitcoin can stay cheap on-chain for an extended period when the macro environment prices out the marginal buyer.

Whether Bitcoin gets the macro conditions of a bottom depends on what happens in Washington over the next seven days.

A major Bitcoin miner burned through 357 BTC on secret compute deals while its output plummeted

Production and managed hashrate fell in July, while the price and economics of the prepaid capacity remain undisclosed.

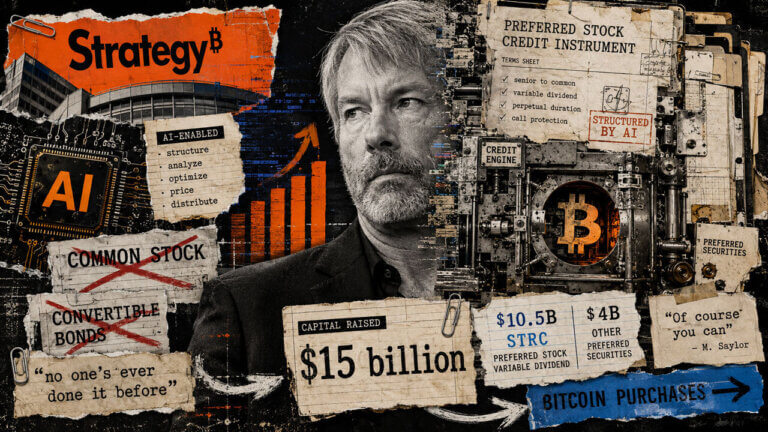

Michael Saylor reveals how ChatGPT helped Strategy unlock $15 billion for its Bitcoin machine

Strategy turned to artificial intelligence to help design unconventional preferred stocks like STRC and STRK.

Never sell treasury model cracks again as 1,635 BTC is offloaded shrinking Empery reserves by 76% in weeks

The company retained 1,279 BTC by Aug. 6, with 954 pledged against $35 million of debt.

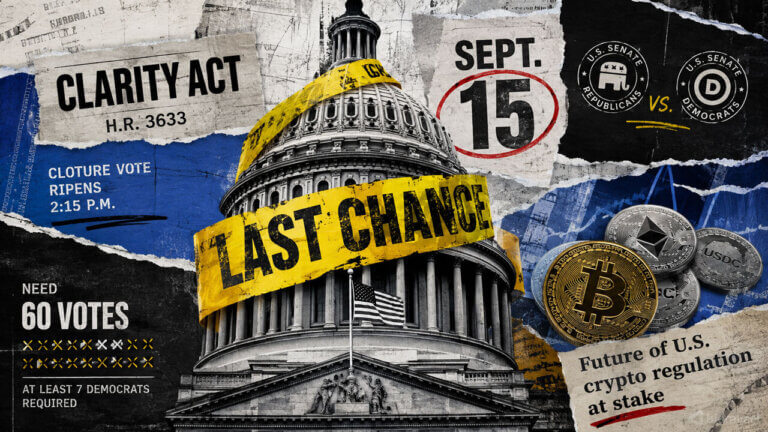

White House warns CLARITY Act will die Sept 15 unless 7 Democrats vote yes

Patrick Witt says lawmakers cannot keep delaying as Republicans declare 11 months of negotiations finished.

AI financial advisers carry a hidden Bitcoin bias activated by a single specific switch

AI models can favor Bitcoin under crisis and machine-economy prompts, exposing a new risk for banks using automated financial advice.

Bitcoin and Ethereum ETFs break $1B in their best week since April and BlackRock brought in 80% of the cash

US crypto ETFs pulled in more than $1 billion, with IBIT and ETHA absorbing roughly $896 million combined.

Bitcoin faces $70,000 breakout or $60,000 drop this weekend as Hormuz tensions rise

Bitcoin enters the weekend with $67,300 as the breakout trigger, $70,000 above, and $60,000 as key support.

Bitcoin holds $64,000 as private hiring drops 53% before today’s macro test that could break support

ADP private-job growth fell to 44,000 from 95,000, but wages and yields resist a simple relief trade.

Bitcoin price breaking out toward $69,000 now opens a turbo path toward $84,000

A Bitcoin breakout above $69,000 could open a thinner supply zone toward $84,000, but Friday’s jobs report and weak ETF demand may decide whether the move holds.