Op-ed: On Bitcoin and why there is no second best – Part 2

A key differentiator with bitcoin in terms of its ability to act as money is the credibility of its monetary policy.

Cover art/illustration via CryptoSlate. Image includes combined content which may include the use of AI tools.

Note: This is part two of a two part series on what differentiates bitcoin from the rest of the crypto market. See part one here.

It could be said that bitcoin will have been nothing more than a Ponzi game if it fails and eventually fades into obscurity. However, this characterization applies to successful, widely-used forms of money as well, as they’re effectively bubbles that haven’t popped. Some forms of money are seen as more credible than others. Still, these similarities between money, bubbles, and Ponzi games can cause a heavy amount of confusion for crypto market participants.

What is clear is that none of the speculative activity happening in the rest of the crypto market can compete with bitcoin as a money or savings mechanism, at least in the traditional sense. Long-term savings necessitates predictability, security, longevity, and a monetary policy that is “set in stone”, and there’s nothing else in the crypto market that comes close to bitcoin in that regard.

The Credibility of Bitcoin’s Monetary Policy

A key differentiator with bitcoin in terms of its ability to act as money is the credibility of its monetary policy. The fact that the rate of issuance of new bitcoin over time will not change is even more important than the often-touted 21 million cap because it is the unwavering nature of the issuance rate that provides the market with a clear understanding of what will happen in the future.

Holders of bitcoin know what they’re getting into when they first buy the crypto asset, and they do not need to worry about outside factors such as the potential inflation in traditional fiat currencies caused by central bankers or supply shocks that lead to unforeseen changes in the prices of commodities in the physical world.

Recently, JPMorgan Chase CEO Jamie Dimon claimed Bitcoin creator Satoshi Nakamoto could reappear one day and inflate the bitcoin supply on a whim; however, this is not possible due to the system's design. While Satoshi could offer a code change to the market, operators of full nodes on the Bitcoin network would have to accept the change en masse. The difficulties associated with making any controversial change were illustrated by the conclusion of the block size wars in 2017 (read more details on that here).

As a side note, one of the main criticisms of the idea that bitcoin’s monetary policy is already set in stone is that there is the potential need for a change to the monetary policy in a situation where transaction fees alone do not offer enough income to miners (as the issuance of new bitcoin in the form of a block subsidy approaches zero), which would weaken the security of the system. However, the general response to this criticism is that bitcoin will already have failed as a money if people are not using it enough to support the system on transaction fees alone.

Most of the money use case has been conceded to bitcoin. Some believe Ether or one of the more currency-focused altcoins, such as Dogecoin, could become money. However, none of these alternatives come close to Bitcoin regarding monetary policy credibility. For example, the level of centralization around Elon Musk found in Dogecoin means that the monetary policy will effectively be whatever he decrees. And when Dogecoin is the closest competitor, it’s safe to say the currency-focused altcoin concept itself is mostly dead.

Additionally, Ether’s monetary policy was just recently changed during the finalization of its move from proof-of-work to proof-of-stake, so it will take a long period for that specific policy to generate its credibility.

Different Strokes: Money vs Tech

Up to this point, the most successful crypto projects outside of bitcoin have acted more as tech stocks than money. Compared to Bitcoin, systems like Ethereum make different tradeoffs in terms of features, centralization, security, and various other factors. Tradeoffs are made in Bitcoin to make it the best possible money, while other platforms are trying to be the best possible platform for the development of decentralized applications, which tends to weaken the credibility of the system’s issuance policy and increase centralization—thus harming utility as a reliable form of savings.

Platforms such as Ethereum, BNB Chain, Tron, and Polygon are more similar to traditional tech stocks, especially when looking at how transaction fees effectively become dividends for stakers of that particular system’s underlying crypto asset. Suppose the platform becomes less useful for stablecoins, non-fungible tokens (NFTs), and decentralized finance (DeFi) applications. In that case, the value of that crypto asset should decline over time (and vice versa). This same framing also applies to DeFi tokens that share revenue with their token holders.

With this perspective of the crypto market, it becomes clear that there is much more competition in this sector than when it comes to bitcoin’s niche use case as money. Firstly, many layer-one blockchains want to be platforms for these decentralized applications.

Secondly, it’s unclear how much it makes sense to publish this sort of activity on a public blockchain in the first place. Part one of this series covers many points of centralization found with these applications that could indicate a more centralized approach at the base layer, whether through a traditional server or a permissioned blockchain, could make more sense. This adds an extra layer of complexity and uncertainty on top of the general lack of credibility in monetary policy when using these crypto assets for long-term savings.

To be clear, this is not to say that there’s anything necessarily wrong with making this sort of investment, much like there’s nothing wrong with owning Amazon or Apple stock. It’s just that, again, this is something different from bitcoin.

While all of these various tech platforms compete with each other, bitcoin stands alone as a new, decentralized form of digital money with an unchanging and trustworthy monetary policy. In other words, there is no second best.

Bitwise pitched a diversified 10-crypto fund, then lost $500 million as Bitcoin swallowed 78% of the portfolio

Market losses and net redemptions cut the fund to $532.8 million while Bitcoin’s portfolio share rose to 77.81%.

Bitcoin’s BIP-110 fork is back, but its backers want to replace the miners and change PoW

Roughnecks is restarting the stalled branch while supporters push a more radical change to Bitcoin’s mining rules.

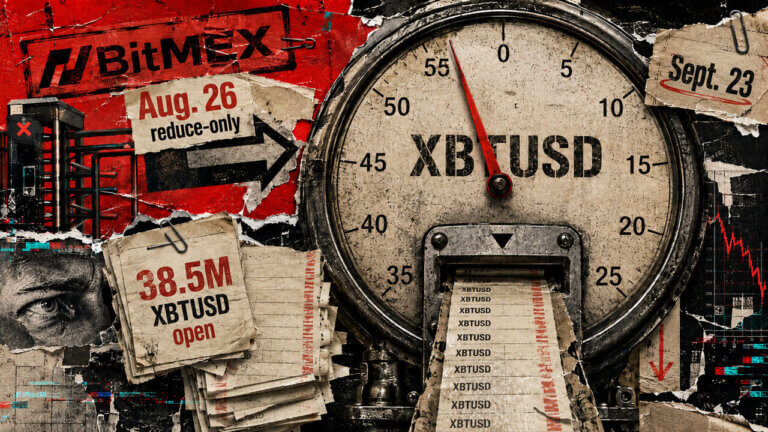

Traders holding $39.5 million in BitMEX Bitcoin perps have 16 days to exit before forced closures begin

New positions stop Aug. 26, while contracts left open face a wind-down that ends in forced closure Sept. 23.

Stablecoin payments are going mainstream. What happens when the recipient needs local currency?

Global dollar liquidity solves only part of the cross-border payment problem. FX, local liquidity and settlement still have to connect the two ends.

You may hate MiCA, but the truth is more complicated than both sides admit

MiCA may strengthen trust and investor protection in Europe’s crypto market, but its high compliance burden could squeeze out early-stage startups before they have a chance to prove themselves.

Spot the crypto scam before you hit send

Microsoft’s latest malware warning shows how clipboard hijackers and fake “loopholes” can reroute crypto transfers, turning a routine send into an irreversible loss.