Stablecoins are becoming a central bank problem hiding in T-bill markets

BIS research puts private dollar tokens closer to sovereign funding markets than the payment-rail debate suggests.

Quick Take

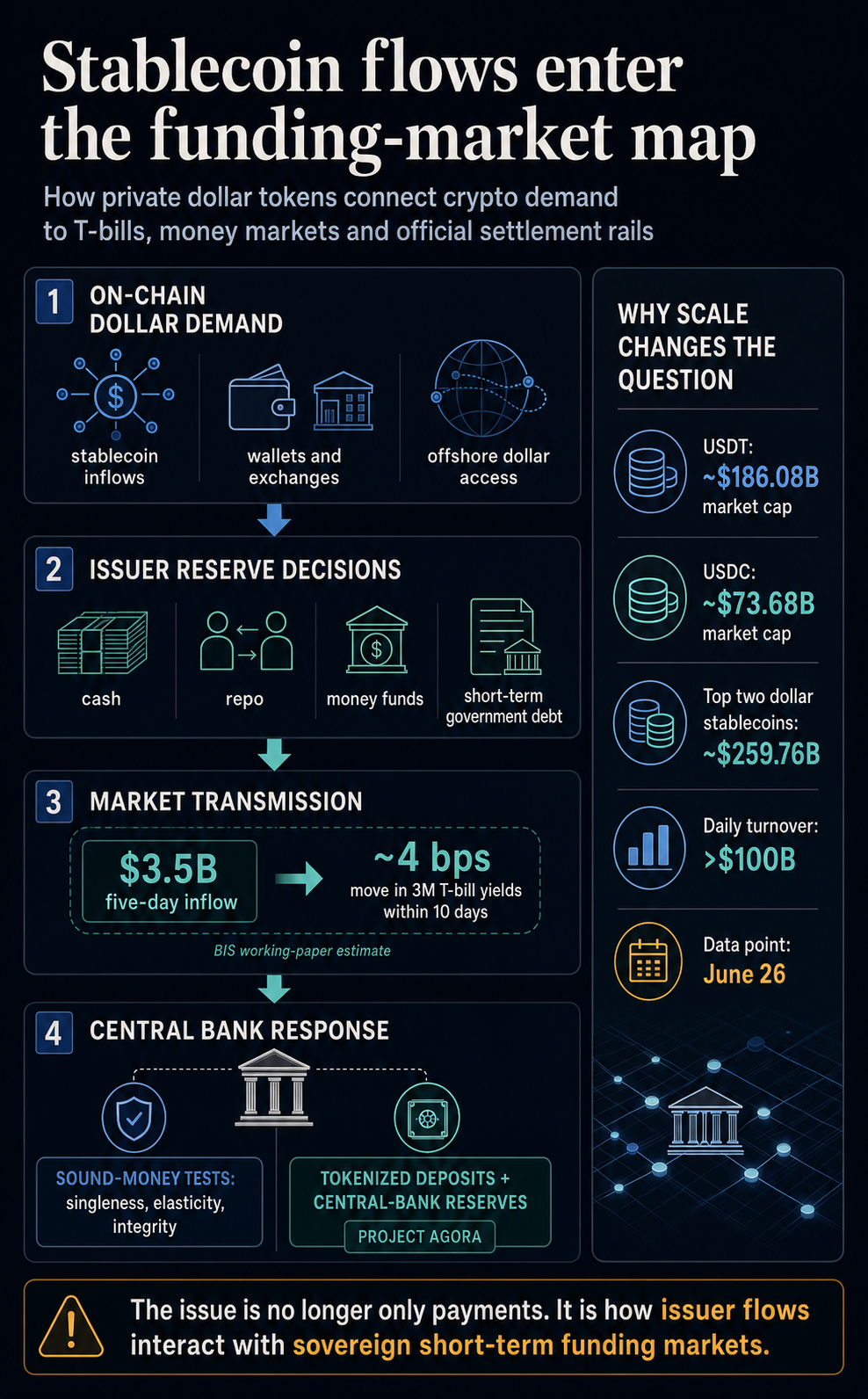

- BIS says stablecoin flows now reach sovereign funding markets, with a $3.5 billion inflow moving three-month Treasury bill yields.

- That makes reserve allocation, redemptions and tokenized settlement a policy issue for central banks, not just a payments debate.

- The open question is whether growth comes from fresh offshore dollar demand or from bank and money-fund balances.

Stablecoin flows have crossed from crypto liquidity into the market map central banks use to track dollar funding.

The Bank for International Settlements, in its June 23 Annual Economic Report chapter on innovation beyond stablecoins, argued that private dollar tokens still fall short of the core tests of money. The same official-sector push now sits alongside a working paper estimate that a $3.5 billion, five-day stablecoin inflow can move three-month Treasury bill yields by about four basis points within 10 days.

The consequence is practical. Stablecoins are becoming a measurable channel between on-chain dollar demand and the front end of sovereign debt markets.

For crypto, stablecoin growth now carries a funding-market signal. For central banks, reserve management, redemption behavior, and tokenized settlement design sit inside the same policy conversation.

The money tests behind the market risk

The BIS chapter starts from a basic monetary test. Money works because users can treat one unit as equal to another, because the system can supply liquidity when payments need to settle, and because the network can control financial crime and preserve trust.

Stablecoins can move fast and can be programmed into public blockchains. BIS acknowledges that utility. Its argument is that current arrangements lack the institutional support needed for bank deposits and central bank money to function as no-questions-asked settlement assets.

In the BIS framework, the weak points are singleness, liquidity elasticity, and integrity. Stablecoins may trade near par most of the time, but they lack the same access to central bank settlement or system-wide liquidity backstops. They can also fragment across chains and venues, making interoperability and financial integrity harder to enforce at scale.

Adoption changes the policy question. A stablecoin used primarily as a crypto quote asset is another. A stablecoin that becomes a large reserve-backed dollar instrument held across exchanges, wallets, and offshore markets is another.

The issuer then has to decide where reserves are held, how redemptions are met, and which assets are bought or sold as demand changes.

The clearest number comes from the BIS working paper on stablecoins and safe asset prices. The paper estimates that a $3.5 billion aggregate stablecoin inflow, about two standard deviations in its sample, lowers three-month Treasury bill yields by roughly 0.71 basis points on impact and up to four basis points within 10 days.

The paper frames the effect as sample-specific rather than a rule for every stablecoin flow. It uses daily data from January 2021 to March 2026, local projections, and an instrument designed to isolate shocks to stablecoin flows.

It also says the estimate is strongest in the maturity bucket where issuers are most likely to hold reserves, and that effects are amplified when Treasury-market intermediaries are under stress or as the stablecoin sector grows.

That is the policy signal in the evidence. A four-basis-point move in a single short-rate instrument is small in isolation. It is still a sign that stablecoin issuers have become large enough for their reserve allocation to show up in the market used to price safe dollar liquidity.

The companion BIS paper on making stablecoins stable(r) adds the other side of the same mechanism. Large redemptions can force issuers to lean on cash buffers or sell short-dated bonds.

The paper models how liquidity and capital thresholds can reduce default and spillover risks when they work as usable buffers, while rigid rules can also push issuers into bond sales too early during stress.

| Stablecoin channel | Market link | Policy signal |

|---|---|---|

| New inflows | More demand for short-term Treasuries or repo | BIS estimates inflow shocks can compress front-end yields where issuer reserves are invested |

| Redemptions | Cash use or bond sales | BIS models show buffers can reduce spillovers, but threshold design can shape stress transmission |

| Foreign demand | Digital dollar access and FX conversion | BIS research links net stablecoin-flow shocks to parity gaps, local currencies and dollar funding premiums |

| Official tokenization | Tokenized deposits and central bank reserves | BIS projects are testing supervised settlement rails inside the two-tier monetary system |

Separate BIS research on stablecoin flows and FX markets extends the point beyond T-bills. It finds that shocks to net stablecoin inflows can widen deviations from stablecoin-dollar parity, affect local currency values, and change short-term dollar funding premiums.

The finding stops short of turning every stablecoin transfer into a macro event. It shows why central banks are studying these flows as part of dollar and FX plumbing.

Scale makes the spillover question harder to ignore

CryptoSlate market data on June 26 showed Tether with a market capitalization of about $186.08 billion and a 24-hour trading volume of about $84.95 billion. USDC stood at a market cap of nearly $73.68 billion and a daily trading volume of $15.54 billion.

Together, the two largest dollar-stablecoins represented roughly $259.76 billion in market value and more than $100 billion in daily trading volume. Stablecoins remain far smaller than the Treasury market, but their reserve portfolios are concentrated in cash, repo, money funds, and short-duration government debt.

The US and European policy backdrop helps explain why the reserve question is arriving now. The White House framed the GENIUS Act around 100% liquid backing, monthly reserve disclosures, and the idea that regulated stablecoins could support demand for Treasuries and the dollar.

That is a policy claim, rather than a market certainty, but it explains why reserve composition has become central.

Europe is asking a similar question from the other side. The European Commission opened a 2026 review of MiCA's crypto-asset framework, including asset-referenced and e-money tokens.

The ECB has also argued that stablecoins have moved to the center of the policy debate as dollar-denominated tokens raise questions about monetary sovereignty and sovereign bond demand.

The live issue is the kind of financial institution issuers become once regulation pushes them toward specific reserve assets, disclosures, redemption rules, and supervisory reporting.

That policy mix leaves central banks with a harder task than approving or rejecting a product category. Reserve rules can improve disclosure, liquidity discipline, and redemption confidence, yet they can also make issuer portfolios easier to read as large funding-market positions.

A regulated stablecoin issuer that buys bills in size during growth and sells or runs down liquid assets during stress is more than a payment company in market terms. It is also a balance sheet whose flows can interact with the instruments used to transmit dollar liquidity.

Tokenized bank money is the official alternative

The chapter's preferred path is to integrate tokenized finance into the existing two-tier monetary system, in which central bank money anchors settlement and regulated private institutions provide services to users.

That is where Project Agora fits. The BIS Innovation Hub project brings together central banks and more than 40 regulated financial institutions to test wholesale cross-border payments using tokenized commercial bank deposits and tokenized central bank reserves on a shared platform.

In a May 27 announcement, BIS said the project has already shown that atomic multi-currency settlement can be executed using tokenized deposits and central bank reserves while preserving the legal character of those instruments.

The next phase is intended to move toward real-value testing.

That is the institutional answer to the stablecoin question. Private stablecoins have shown that users want programmable dollar instruments that move across digital venues. Central banks are now testing whether the same functions can be delivered through tokenized deposits and central bank settlement assets without losing the safeguards that make money work under stress.

For crypto markets, the consequence reaches beyond tighter stablecoin regulation. If issuers are large reserve managers, then inflows, redemptions, and asset allocation become funding-market signals.

If tokenized deposits gain traction, stablecoins face competition from a model that offers programmability without leaving the banking and central-bank settlement perimeter.

The next thing to watch is whether stablecoin growth comes mainly from new offshore demand for digital dollars or from balances that would otherwise sit in banks and money funds.

The first path could deepen demand for short-end dollar assets while extending the dollar's reach. The second could make redemptions, reserve sales, and bank-funding shifts more important in stress.

Either way, the debate has moved. Stablecoins are still payment tokens for users and liquidity rails for crypto venues. They are also becoming part of the machinery through which dollar demand reaches sovereign debt markets.

That is why central banks are treating them as more than crypto plumbing.