Overview

Introduction

You can borrow millions of dollars in crypto with no collateral, no credit check, and no lender waiting to be repaid. The catch? You have to give it all back in the same instant you took it.

That's a flash loan. It's a no-collateral DeFi loan that lives and dies inside one blockchain transaction. If the money isn't returned before the transaction closes, the whole thing gets reversed, as if it never happened.

That one rule changes everything. There's no paperwork, no bank, and no lender chasing a borrower. The smart contract handles repayment automatically. If the math doesn't add up, the chain cancels the transaction and the lender's funds come straight back.

Sounds clean, but it creates its own problems. Flash loans are developer tools, not consumer credit. The mechanism itself is legitimate. But it's also been used to drain weak DeFi protocols, and the internet is packed with “flash loan bot” offers designed to empty wallets rather than generate profit. So what's actually going on here?

Key Takeaways

- A flash loan lets a contract borrow temporary liquidity without collateral for one transaction.

- It lets developers combine borrowing, swaps, liquidations, and repayment into one automated DeFi action.

- The loan reverts if unpaid, but temporary capital can still expose weak or malicious smart contracts.

What Are Flash Loans in Crypto?

A flash loan is a temporary loan controlled entirely by smart-contract logic. The borrower posts no collateral because the loan can't survive beyond the transaction that created it.

That's how the lender stays protected. If the borrower contract can't repay the borrowed amount plus the required fee, the transaction reverts. The lender doesn't chase anyone. The borrower carries no debt. The trade-off is that the loan only works when the borrowed assets can be used and repaid inside the same execution path, which rules out most everyday uses of money.

A flash loan can't pay a bill, fund a wallet for later spending, or move money off-chain. It only helps when an entire strategy, borrow, act, repay, fits inside one transaction. Most flash loan activity happens inside DeFi lending pools, decentralized exchanges, liquidations, collateral swaps, and automated strategies.

For beginners, the clearest way to think about it: a flash loan is a mechanism for temporary transaction liquidity. It is not a shortcut to free money, and it is not consumer credit. The smart contract is the only enforcement mechanism, and it enforces one rule — pay it back in time, or nothing happens at all.

How a Flash Loan Works in One Transaction

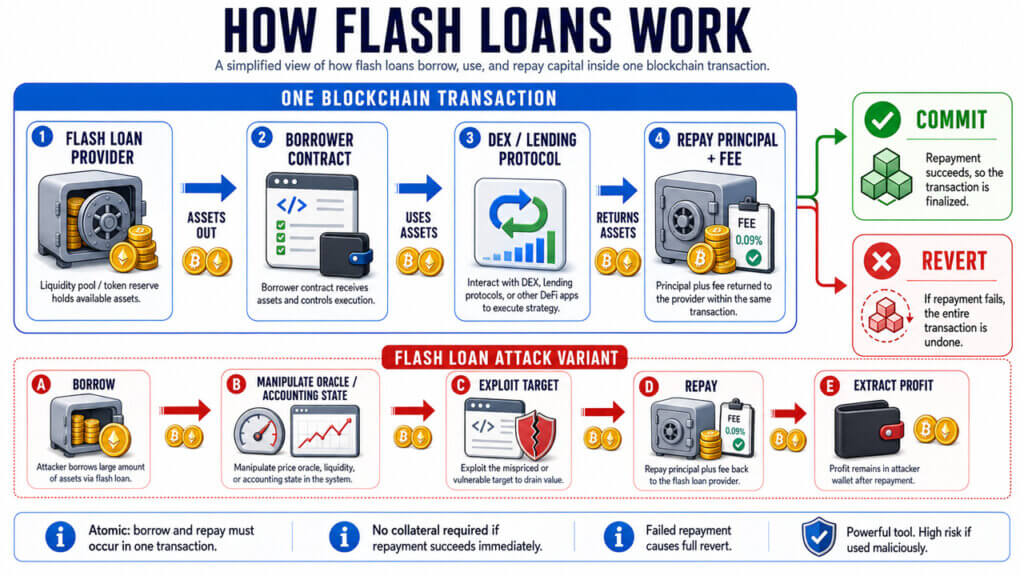

A flash loan wraps borrowing, use, repayment, and validation into one atomic transaction. Atomic means the chain keeps the whole transaction only if every required step succeeds. If any step fails, including repayment, the entire transaction gets reversed.

The borrower is usually a smart contract, not a normal wallet click. On Aave V3, for example, the Pool contract handles flash loans. The receiver contract must approve repayment of the borrowed amount plus the fee, or the transaction reverts.

| Step | What Happens |

|---|---|

| Request | A borrower contract asks a flash loan provider for a specific asset and amount. |

| Transfer | The provider sends the assets to the receiver contract. |

| Action | The receiver contract performs the planned swaps, liquidation, collateral change, or other DeFi calls. |

| Repayment | The receiver approves or returns principal plus the fee. |

| Validation | The provider checks repayment and the chain either commits the transaction or reverts it. |

The lender can offer no-collateral liquidity because it relies on transaction finality, not borrower trust. If the last step fails, the earlier transfer gets unwound along with the rest of the transaction state.

That's also what makes flash loans hard for beginners to use. The useful part isn't the borrowing itself. It's the exact sequence of contract calls that has to sit between the loan and the repayment. Writing that sequence requires understanding smart contracts, gas behavior, DeFi protocols, and execution timing all at once. None of that is visible in a “paste this code and profit” tutorial.

Everything depends on the transaction boundary. Funds enter the borrower contract, the contract performs one or more DeFi actions, repayment plus fee returns to the provider, and the chain keeps the whole transaction only if every step succeeds.

Why Borrow Money You Have to Pay Back Immediately?

The point isn't to hold the money. It's to use borrowed capital to execute an action that already has a repayment path built in. Flash loans exist because some opportunities in DeFi require capital you don't have, but can generate enough return to repay that capital within the same transaction.

Arbitrage is the clearest example. Say ETH is trading at $2,000 on one DEX and $2,050 on another. To capture that $50 gap, you'd normally need to already own ETH. A flash loan removes that requirement, but only if both the buy and the sell are encoded into the same transaction and execute atomically. There's no window where you're holding ETH and waiting. Both legs either complete successfully or the whole transaction reverts.

That revert protects the lender, not the borrower. If the second leg can't execute at a profitable price, the transaction fails before it settles. The lender's funds return automatically. You don't end up holding ETH at a loss, but you do lose the gas fees for the failed transaction. On Ethereum mainnet, that cost is real, and it adds up across multiple failed attempts.

The same logic applies to liquidations. A liquidator can use a flash loan to repay someone's undercollateralized debt, claim the collateral reward, sell it, and repay the loan, without holding any capital upfront. Again, if the numbers don't work, the transaction reverts and the liquidator loses gas, not principal.

That's the actual value: flash loans let you act on opportunities that require capital you don't own, as long as the full repayment path is built into the transaction before it runs. The loan is the tool. The opportunity, and the gas risk, belong to the borrower.

Flash Loans vs Traditional Crypto Loans

People often confuse flash loans with regular crypto loans. The two products share a name and almost nothing else.

A traditional crypto loan exists over time. You post collateral, borrow funds, use them however you want, and pay back over days, months, or years. A flash loan must finish inside the transaction that creates it. There's no ongoing relationship, no collateral sitting locked somewhere, and no way to use the funds outside the transaction path.

| Flash Loan | Traditional or Crypto-Backed Loan |

|---|---|

| No upfront collateral is required when the transaction repays in full. | Collateral, credit checks, or account controls usually support the loan. |

| The loan exists only during one blockchain transaction. | The loan can last for days, months, or years. |

| Funds must stay inside the transaction path. | Funds can usually be withdrawn, spent, or moved elsewhere. |

| Failure normally reverts the transaction. | Failure can create liquidation, collections, fees, or default risk. |

The confusion starts with the word “loan.” A flash loan is really temporary execution liquidity. It helps a contract perform a specific action that already has a repayment path baked in. It can't fund anything that doesn't.

What Flash Loans Are Used For

Flash loans don't have many use cases. But the ones they have are genuinely hard to accomplish any other way. They let liquidators, active borrowers, and protocol managers make capital-heavy moves without needing to hold that capital.

Here are the main uses, broken down by what problem they solve:

- Arbitrage between pools, when the price gap is wide enough to cover fees, slippage, and gas.

- Liquidation of unhealthy DeFi loans, when the collateral reward covers the cost of executing the liquidation.

- Self-liquidation, where a borrower uses temporary liquidity to close or shrink a risky position before it gets liquidated at a penalty.

- Collateral swaps, where someone changes the asset backing a loan inside one transaction without unwinding the whole position.

- Debt refinancing, where a loan gets repaid on one protocol and reopened on another in a single step.

- Batch operations, where several DeFi actions are cheaper or safer when grouped into one atomic transaction.

All of these depend on liquid markets. Thin pools move too much during execution. Slippage eats the expected profit before the transaction settles. Flash loan strategies are only as reliable as the pools, oracles, and protocols they touch.

Why Flash Loan Arbitrage Is Not Easy Money

Flash loan arbitrage sounds like a money machine. Borrow free capital, pocket the spread, repeat. In reality, it's a competitive, technical game where beginners rarely survive their first few attempts.

Profitable price gaps are visible to hundreds of bots at once. By the time a beginner sets up their first strategy, automated systems have already competed that spread down to almost nothing. The easy trades are gone.

Then there's the cost problem. Gas, protocol fees, failed transactions, slippage, and MEV competition, where other miners or bots front-run or reorder your transaction, can all eat into or reverse a theoretical profit. A failed flash loan doesn't leave a debt, but it does waste gas. Multiple failures in a row add up to real money lost.

The bigger danger, though, is fake tooling. A huge number of “flash loan crypto bot” offers online are not arbitrage tools. They're wallet drains. The workflow usually looks like this: paste some Solidity code into Remix (a browser-based code editor), fund a contract with some ETH to “activate” it, and approve token permissions. What actually happens is the user's deposit moves to an attacker's wallet, and no flash loan ever runs.

Watch for these patterns before interacting with any flash loan contract:

- The source code is copied from a YouTube video with no explanation of what it does.

- The strategy needs a user deposit before it will “activate” or “start.”

- The contract requests unlimited token approvals.

- The profit estimate ignores gas costs and failed attempts entirely.

- The tutorial never names the specific DEXs, tokens, or repayment path it uses.

- The same contract appears on multiple disposable websites or Telegram channels.

Real flash loan strategies are built by developers who understand contract execution, gas behavior, private order flow, and pool depth. Profit exists, but it comes from that infrastructure, not from a script someone posted in a video description.

How Flash Loan Attacks Actually Happen

A flash loan attack doesn't exploit the flash loan itself. It exploits a flaw in another protocol, and uses a flash loan to make that flaw catastrophic.

The basic pattern: borrow a huge amount, use it to break an assumption the target protocol makes, extract value, repay the loan, and keep the profit. The flash loan just makes the attack cheap. The attacker never needs to own the capital they're using.

OWASP Smart Contract Security classifies flash loan-facilitated attacks as a smart-contract risk, because large temporary balances can violate assumptions about normal position sizes, capital exposure, or economic behavior.

Here are the weak assumptions attackers most commonly exploit:

| Weak Assumption | How Temporary Capital Abuses It |

|---|---|

| Spot price equals fair price. | The attacker moves a thin pool, triggers a bad valuation, then lets the price normalize. |

| Share accounting cannot be skewed quickly. | The attacker changes deposits, withdrawals, or rounding paths at unusual scale. |

| Governance weight reflects durable ownership. | The attacker borrows voting power or balance influence for a short window. |

| Liquidation math handles every edge case. | The attacker creates an extreme position and routes through a profitable liquidation path. |

| One protocol can trust another protocol's instant state. | The attacker changes the external state long enough for the target to read it. |

Oracle design is one of the main defenses here. An oracle is a service that feeds real-world price data into a blockchain protocol. A protocol that prices collateral using a single shallow pool is extremely easy to manipulate. One that pulls from multiple independent data sources, with checks for stale or extreme values, is much harder to break.

The Euler Finance incident is the clearest real example. Chainalysis reported that Euler lost roughly $197 million in March 2023, with the stolen funds later returned. The flaw was in Euler's donation and liquidation logic, not the flash loan protocol. Instant borrowed capital turned that logic flaw into a protocol-wide loss.

Flash Loan Risk Checks for DeFi Users and Builders

Most DeFi users will never take a flash loan. But they can still be hurt by one.

If you deposit funds into a protocol with weak oracle design, fragile accounting, or no emergency pause controls, a flash loan attack against that protocol becomes your problem. You didn't do anything wrong. You just picked the wrong place to put your money.

The most practical user-side protections are:

- Use protocols with clear audit reports, active bug bounties, and a documented history of responding to incidents.

- Avoid new or thinly traded pools where one large trade can move the price sharply.

- Review what token approvals you've given before and after using new DeFi tools.

- Be skeptical of vaults that claim automated flash loan yield without explaining the strategy clearly.

- Don't deposit funds to test any contract shared in a video, a chat group, or a social post.

Builders face a different set of problems. Their code becomes the attack surface. Strong protocol design means treating flash-loan-scale capital as a permanent threat, not an edge case.

Key controls for protocol builders:

- Use time-weighted average prices (TWAPs) and multiple data sources for oracles, not single-pool spot prices.

- Cap the amount of state that can change inside one transaction.

- Test liquidation paths, share math, collateral ratios, and rounding logic under flash-loan-sized inputs.

- Build circuit breakers that trigger on abnormal price moves or sudden liquidity shifts.

- Run audits that include economic attack simulations, not just code review.

- Keep pause controls active and a response process ready before material funds are at risk.

None of these eliminate DeFi risk entirely. But they shrink the window between “temporary borrowed capital” and “permanent protocol damage.”

Flash Loan Platforms, Fees, and Standards

If you are also looking for the best flash loan crypto platform, remember that comparison of flash loan providers is not that easy. The protocol, asset availability, fee model, and contract interface all differ — and any of them can affect whether a strategy works.

Aave is the most widely referenced example. Aave V3 exposes flashLoan() for multi-asset borrowing and flashLoanSimple() for a single asset. Its flash loan fee is initialized at 0.05%, with governance able to update it.

If you also want to participate in this activity, this list of the top DEXs can help you get started.

| Provider or Standard | What to Know |

|---|---|

| Aave V3 | Uses Pool-based flash loan functions and receiver contracts that repay principal plus fees. |

| Uniswap V2 Flash Swaps | Let a contract receive assets and pay for them later in the same transaction, as described in the Uniswap V2 whitepaper. |

| Balancer V2 Vault | Uses consolidated Vault liquidity for flash loans that revert if repayment fails, based on Balancer's flash loan workflow. |

| ERC-3156 | Standardizes a single-asset flash loan interface with lender and receiver callbacks. |

| dYdX | Appears in older flash-loan examples, but current integrations should verify the active product and interface before relying on old tutorials. |

ERC-3156 is the standard worth understanding if you're a developer. It defines a shared callback pattern for lender and receiver behavior: the lender transfers assets, calls the receiver, and collects the amount plus fee, or reverts. Protocols built to this standard are far easier to integrate consistently than custom implementations.

For dYdX, older SoloMargin examples should be verified against current documentation before reuse. Old tutorials often assume an interface from a deprecated product version.

No table can rank providers by profit. Profit depends on asset depth, gas, block ordering, contract design, and whether the opportunity even still exists when your transaction lands.

How to Use Flash Loans Without Falling for Bot Scams

The safest rule is simple: never fund a flash loan contract before you fully understand what it does. Any tutorial that needs real money before you understand the mechanism isn't teaching you anything. It's setting you up to lose your deposit.

Flash loan scams almost never involve an actual flash loan. The scam lives in the approval workflow. The user grants a token permission, the contract drains the wallet, and no borrowing ever happens.

Before you touch any flash loan code or tool, go through this list:

- Read official protocol documentation before any third-party tutorial or video.

- Practice on a testnet or local fork before touching mainnet.

- Never paste unknown Solidity into Remix with a funded wallet attached.

- Don't trust contracts that promise fixed or “guaranteed” profit.

- Check your token approvals regularly and revoke permissions you no longer need.

- Learn how gas works, how DEX pools price assets, what slippage means, and what a transaction revert looks like, before you look at any bot.

Flash loans themselves are not a scam. The scam is always in the wrapper: fake websites, recycled contract code, wallet-draining approvals, and profit projections that quietly leave out gas costs and failed attempts.

FAQs

Can anyone get a flash loan?

Anyone can call a protocol that offers flash loans if they meet the protocol’s contract requirements, but that doesn’t mean every wallet user can use one safely. Most practical flash loans require a smart contract, a defined strategy, repayment logic, and enough gas to execute the full transaction.

What happens if a flash loan is not repaid?

If repayment fails, the transaction normally reverts and the loan is unwound with the rest of the transaction state. The borrower typically loses gas, not the borrowed principal, because the chain does not keep the failed state.

Are flash loans a scam?

Flash loans are legitimate DeFi tools, but many profit-bot offers built around them are scams. Be especially careful when a tutorial asks you to paste code, fund a contract, or grant broad token approvals before explaining what the contract actually does.

Can you make money with flash loan arbitrage?

Flash loan arbitrage can be profitable for skilled developers, but it requires real infrastructure — not copied scripts. Fees, gas, slippage, failed transactions, and MEV competition can erase a visible price difference before a transaction settles.

What is the difference between a flash loan and a flash loan attack?

A flash loan is the temporary borrowing mechanism. A flash loan attack uses that temporary capital to exploit a weak oracle, accounting rule, governance path, collateral check, or other smart-contract assumption in a target protocol.

Do flash loans require coding?

Most serious flash loan use requires coding because the transaction needs custom logic for borrowing, execution, repayment, and failure handling. No-code interfaces may exist, but users should treat profit claims and unknown contract approvals with caution regardless of how the tool is presented.