The FCA Cryptoasset Business Registration Regime is the United Kingdom’s in-force anti-money laundering and counter-terrorist financing framework for certain cryptoasset businesses under the Money Laundering Regulations 2017, as amended. The crypto-specific gateway has applied since 10 January 2020. As of 19 June 2026, an in-scope cryptoasset exchange provider or custodian wallet provider carrying on business in the UK generally must be registered with the Financial Conduct Authority before beginning those services. A separate FCA authorisation or registration for another financial service does not replace the MLR registration.

Registration is limited to AML/CTF supervision. The FCA states that it is a legal requirement, not an endorsement or recommendation of the business, and it should not be presented as equivalent to full authorisation under the Financial Services and Markets Act 2000.

Who the FCA cryptoasset registration regime covers

The exchange-provider definition includes exchanging cryptoassets for money, money for cryptoassets or one cryptoasset for another; arranging those exchanges; and operating cryptoasset ATMs. It can also capture creators or issuers when they provide those services. The custodian-wallet definition covers safeguarding customer cryptoassets, or safeguarding and administering private cryptographic keys used to hold, store or transfer cryptoassets.

The territorial test focuses on business carried on in the UK. A UK office, head office or crypto ATM may indicate UK activity. The FCA says that merely serving a UK client, without a UK office or other UK activity, does not automatically mean the business is carried on in the UK. The separate financial-promotions regime may nevertheless apply to marketing directed at UK consumers regardless of where the firm is based.

Core registration and AML/CTF requirements

The FCA assesses the applicant, relevant officers, managers and beneficial owners under the MLR fit-and-proper test. The statutory framework permits refusal where requirements are not met or information is materially false or misleading, and gives the FCA three months to determine a complete cryptoasset registration application before any representations process.

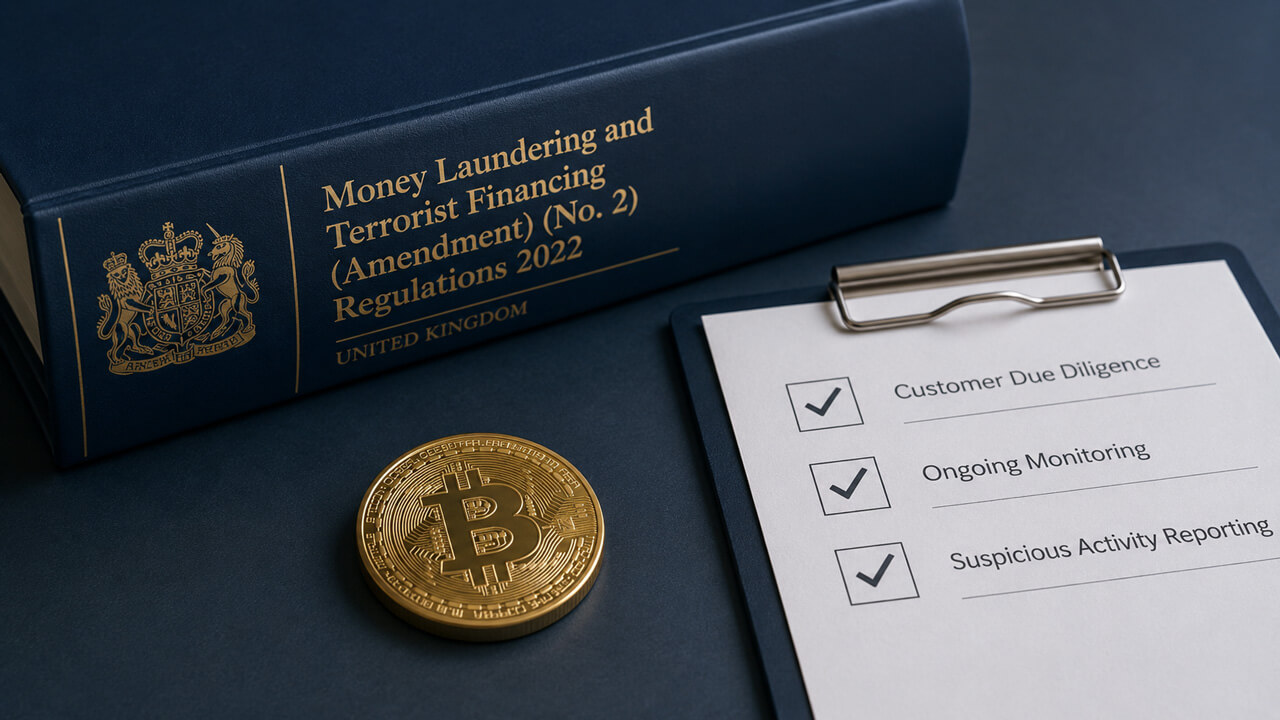

Registered firms remain subject to ongoing, risk-based obligations rather than a one-time filing. Expected controls include a business-wide risk assessment, customer risk assessments, customer and enhanced due diligence, sanctions and politically exposed person screening, transaction monitoring, training, suspicious activity reporting, record-keeping, outsourcing oversight and an appointed money laundering reporting officer. The FCA expects systems and policies to be tailored to the firm’s business model and to address both on-chain and off-chain activity where relevant.

Travel Rule and 2026 MLR amendments

Since 1 September 2023, Part 7A of the MLRs has imposed cryptoasset transfer-information duties commonly called the Travel Rule. Depending on the transfer, originator and beneficiary names, account numbers or unique transaction identifiers, and additional identifying information may need to accompany the transfer. The framework also addresses verification, missing information, intermediaries, unhosted wallets, retention and disclosure to law enforcement.

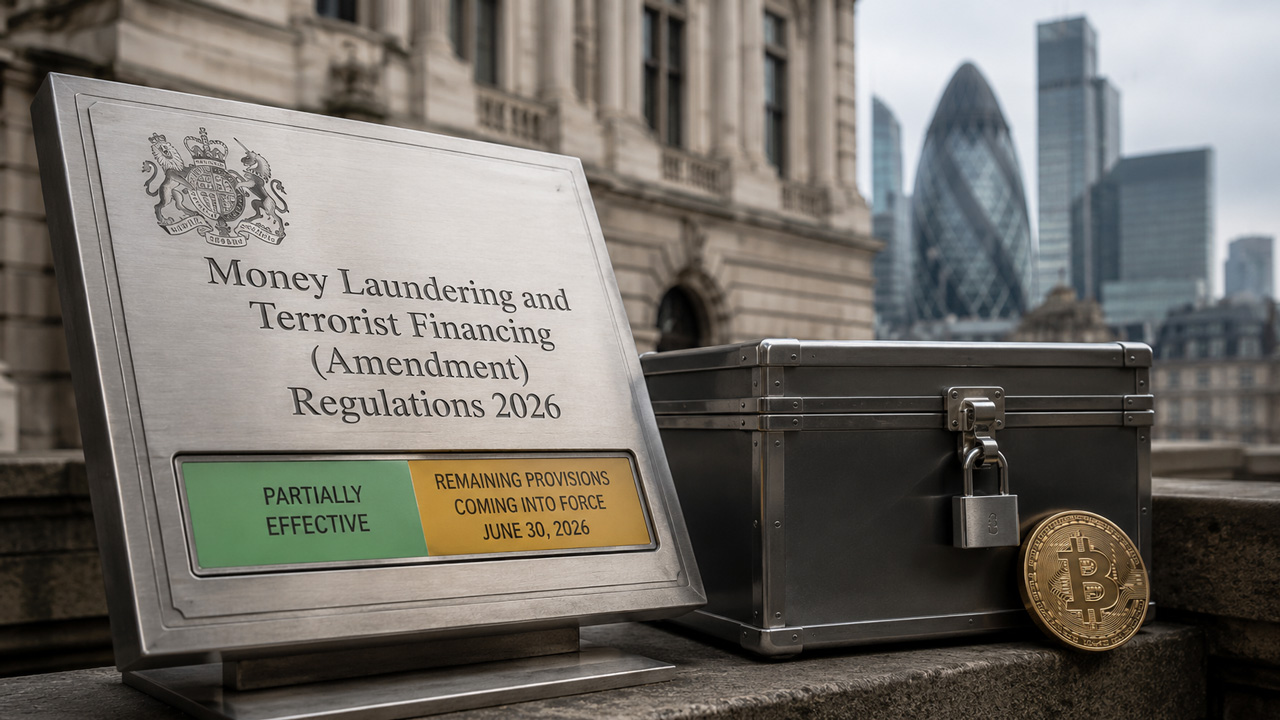

The Money Laundering and Terrorist Financing (Amendment) Regulations 2026 were made on 9 June 2026. Most provisions commence on 30 June 2026. Crypto-specific enhanced due diligence for certain correspondent relationships starts on 1 February 2027, while elements of the revised change-in-control schedule take effect in stages through 25 October 2027.

Transition to the UK FSMA crypto regime

MLR registration remains operative during the transition to the broader FSMA cryptoasset regime. The FCA’s FSMA application window runs from 30 September 2026 to 28 February 2027, and the new regime is scheduled to start on 25 October 2027. MLR registration does not convert into, or guarantee, FSMA authorisation.

On full commencement, the 2026 Cryptoassets Regulations restructure the MLR register so that authorised cryptoasset firms and specified-investment cryptoasset firms are excluded from that register and instead follow a notification route. The MLR gateway will continue for businesses that remain within its scope and do not fall within those exclusions. The change is therefore a transition and reconfiguration of the AML registration framework, not a blanket repeal of the MLR obligations.

This profile is a general legal-reference summary and does not constitute legal advice.